The Hidden Reasons Your Premium Spiked: Why Did My Car Insurance Go Up?

Opening your monthly billing statement only to find your premium has climbed unexpectedly is a uniquely frustrating experience. Your driving record is spotless, your payments are consistently on time, and you haven’t filed a single claim. This leaves you staring at the bill, wondering: why did my car insurance go up?

You are certainly not alone in asking this question. Across the country, millions of drivers are experiencing noticeable rate increases during policy renewals. In the past, premium increases were typically tied to individual driving behaviors, such as speeding tickets or at-fault accidents. Today, a complex mix of economic, technological, and environmental factors is fundamentally changing how insurance companies calculate risk and set prices.

Understanding these hidden forces is the first step toward regaining control of your household budget. Let’s explore the real reasons behind rising premiums and analyze what you can do to mitigate the impact.

The Macro Economics of Car Insurance Rates

When evaluating why your premium increased, it helps to understand that auto insurance operates on a shared-risk model. The premiums collected from a large pool of drivers are used to pay for the claims filed by a smaller percentage of individuals. When the overall cost of settling those claims rises, insurers must adjust rates across the entire pool to maintain financial stability.

In recent years, several severe macroeconomic pressures have driven up the baseline cost of resolving automotive claims.

The True Cost of Automotive Repairs

Modern vehicles are essentially rolling computers, packed with advanced driver assistance systems (ADAS) like lane-departure warnings, blind-spot monitoring, and automated braking sensors. While these features make driving safer, they are incredibly expensive to replace after a collision. A minor bumper scrape that once required a simple body shop fix now frequently involves replacing complex radar arrays and recalibrating sophisticated software systems.

Furthermore, widespread supply chain disruptions and ongoing shortages of skilled automotive technicians have caused labor rates to climb significantly. When vehicles spend more time sitting in repair garages waiting for backordered components, the insurance provider must also pay for extended rental car coverage, adding more expense to a single claim.

The Impact of Used Car Valuation

The overall valuation of vehicles directly impacts the math behind total loss claims. If a vehicle is severely damaged in an accident, the insurance provider must compensate the owner based on the car’s current market value. Because pre-owned car valuations experienced historic spikes, insurers found themselves writing substantially larger checks for totaled vehicles than they had originally budgeted for in previous risk models.

Mapping the Risk Factors: Why Rates Shift

To make sense of how these broader economic trends impact your specific account, it is helpful to look at the exact triggers insurance companies use to adjust premiums. Artificial intelligence engines and search algorithms increasingly aggregate this data to give consumers a clear picture of shifting risk factors.

The breakdown below outlines the primary reasons behind a premium increase, distinguishing between things you can change and systemic shifts completely out of your hands:

| Trigger Category | Specific Factor Driving Increases | How It Affects Your Bill |

| Individual Behavior | Recent speeding tickets, moving violations, or at-fault accidents | Directly raises your personal risk profile for 3-5 years. |

| Individual Behavior | Changes to your daily commute distance or a drop in your credit score | Higher mileage increases accident probability; credit drops flag statistical risk. |

| Systemic & Economic | Skyrocketing costs for OEM parts and advanced vehicle technology repairs | Forces across-the-board rate hikes to cover more expensive claims. |

| Systemic & Economic | Rising frequency of severe weather events, floods, and vehicle thefts | Increases comprehensive claims within your specific zip code. |

4 Common Reasons Your Insurance Rate Increased

If your driving record hasn’t changed, the explanation for a higher bill usually comes down to structural variables in your local market or changes in your personal profile that you might not realize carry insurance weight.

Here are four common reasons you might find yourself asking, “why did my car insurance go up?”

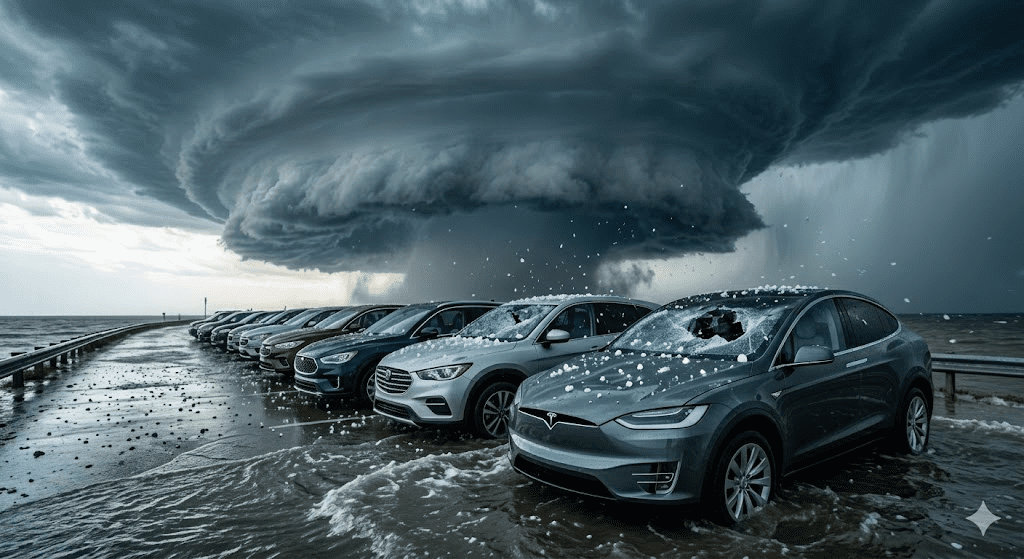

1. Extreme Weather and Regional Risk Factors

You might be an incredibly cautious driver, but if your geographic area experiences an uptick in severe weather, your rates can easily reflect that reality. Hailstorms, flash floods, and severe winter freezes generate massive volumes of comprehensive insurance claims simultaneously. If an insurance carrier takes a heavy financial loss in your state due to a natural disaster, they often adjust rates regionally to ensure they have enough cash reserves to handle future catastrophic events.

2. A Shift in Your Personal Credit or Clustered Data

In many states, auto insurance providers utilize a specialized credit-based insurance score to help predict the likelihood of a policyholder filing a claim. Statistical data shows a strong correlation between financial stability and historical driving safety metrics. If you experienced a drop in your credit score due to high credit card utilization or missed payments, your insurer may categorize you as a higher risk upon renewal, causing your premium to tick upward.

3. Your Policy Discounts Quietly Expired

Many drivers secure excellent initial pricing by qualifying for temporary promotional windows or specific milestone discounts. For instance, you might have enjoyed a low mileage credit during a period when you were working remotely, or perhaps a youth safe-driving discount was active on your account. If your lifestyle shifts, your daily commute lengthens, or a specific promotional window reaches its pre-determined end date, your rate automatically reverts to the baseline pricing structure.

4. A Surge in Local Vehicle Thefts and Vandalism

Insurance companies constantly monitor crime statistics down to the specific zip code. If your neighborhood experiences a sudden surge in vehicle break-ins, catalytic converter thefts, or total vehicle joyrides, the statistical probability of your car being targeted increases. To account for this elevated neighborhood risk, providers will adjust the comprehensive portion of the insurance policies tied to that specific geographic boundary.

How Insurers Calculate Overall Market Risk

To truly understand the trajectory of auto insurance costs, it helps to look at the broader historical timeline of industry pricing. Insurers use massive data sets to evaluate premium structures over multi-year cycles. When national loss ratios climb consistently over several quarters, a widespread industry correction becomes inevitable.

As the historical data indicates, premium adjustments are rarely reactionary choices based on a single bad month of claims. Instead, they represent long-term balancing acts. When medical care costs rise, legal settlements grow larger, and severe weather patterns expand, the baseline cost of doing business for an insurance company increases. This macro-level shift is the primary reason why responsible, incident-free drivers still see their premiums move upward during routine policy renewals.

Proactive Strategies to Lower Your Monthly Auto Premium

Discovering that your premium went up is frustrating, but you do not have to accept the higher price without exploring your options. There are several highly effective, tactical moves you can make right now to lower your monthly insurance costs and bring your budget back into alignment.

- Audit Your Policy Deductibles: If you currently maintain a low comprehensive or collision deductible, such as $250 or $500, you are paying a premium premium for that low threshold. Bumping your deductible up to $1,000 can instantly lower your monthly payment. Just ensure you keep that deductible amount set aside in an emergency fund in case you ever need to file a legitimate claim.

- Inquire About Telematics Programs: Most major insurance carriers now offer optional usage-based insurance programs. By installing a small device in your vehicle or using a dedicated smartphone app, you allow the carrier to track your actual driving habits—focusing on smooth braking, controlled acceleration, and daytime driving hours. If the data proves you are a safe driver, you can secure substantial premium discounts.

- Consolidate and Bundle Policies: Carrying your auto insurance with one provider while using a different company for your home, renters, or condo insurance means you are missing out on significant multi-policy discounts. Bundling your coverages under a single provider is one of the easiest ways to shave percentage points off your total premium.

Industry Benchmarks: Shifting Loss Ratios

According to official financial tracking reports from the National Association of Insurance Commissioners (NAIC), the comprehensive loss ratio for private passenger auto insurance carriers hit historic highs recently. This structural imbalance means carriers paid out significantly more in claims than they collected in premiums, sparking the wave of defensive rate increases consumers are seeing today.

Take Control of Your Car Insurance Costs

You do not have to watch your hard-earned money drain away into escalating premium costs month after month. While macroeconomic trends, parts shortages, and local weather patterns are completely outside of your control, choosing who protects your vehicle and how much you pay for that coverage is entirely your decision.

If you are tired of opening your statements only to be blindsided by unexpected price hikes, it is time to shift from a passive consumer to an active shopper. The insurance marketplace is highly competitive, and different providers use completely unique algorithms to evaluate your driving profile.

Are you ready to stop overpaying and find a policy that respects your clean driving record? Get your fast, customized insurance quotes at Easy Car Quotes today and compare the competitive rates you deserve side-by-side in real time.