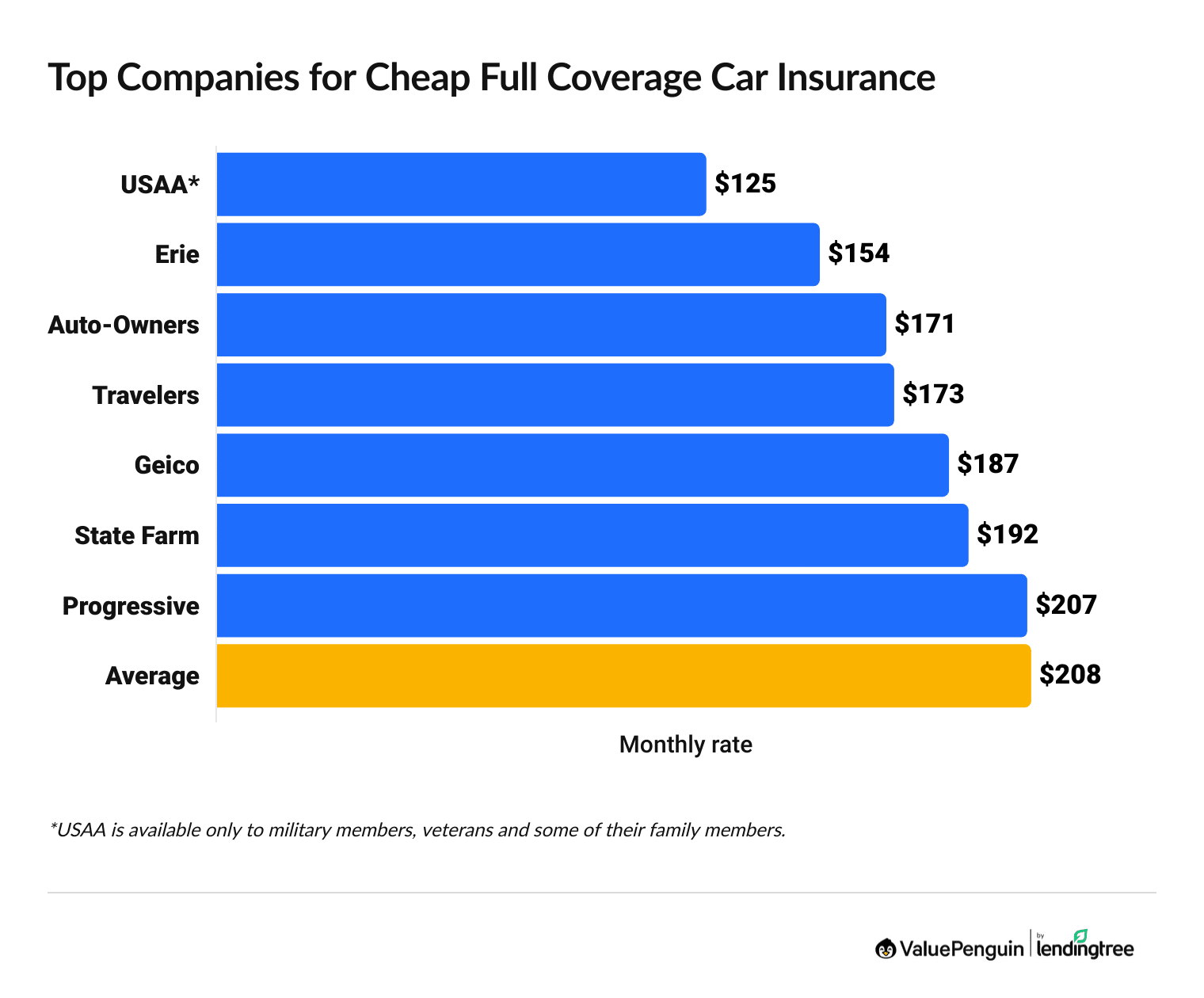

The Reluctant Adult’s Guide to the Best Affordable Car Insurance

Let’s be honest: shopping for car insurance ranks somewhere between “getting a root canal” and “accidentally hitting ‘Reply All’ on a venting email about your boss” on the list of things people actually want to do. We all know we need it, but watching those monthly premiums vanish from your bank account feels like paying a subscription fee for a club you hope you never actually have to visit.

However, finding the best affordable car insurance isn’t just about picking the lowest number on a screen. It’s about outsmarting the algorithms, understanding the “boring” legal stuff, and ensuring that if a rogue shopping cart decides to wage war on your passenger door, you aren’t left holding the bag.

Why Your Current Rate Is Probably Lying to You

Most people set their insurance on autopilot. You signed up three years ago, the autopay hits every month, and you assume that because you haven’t had a ticket, you’re getting a deal.

The reality? Insurance companies use “price optimization.” This is a fancy way of saying they track how likely you are to shop around. If you stay with the same provider for years without questioning your rate, they might incrementally nudge your premiums up, assuming you’re too busy (or too lazy) to check the competition.

The Secret Menu of Discounts

To land the best affordable car insurance, you have to look for the “secret menu” of discounts. Most carriers won’t just hand these to you; you have to ask.

- The “Telematics” Gamble: If you’re a “grandma driver” (i.e., you actually stop at yellow lights), using a plug-in device or an app can slash your rates by up to 30%.

- The Professional Pivot: Are you an educator? Military? A scientist? Certain professions are statistically less likely to get into high-speed chases with the police. Mention your job; it matters.

- The Credit Score Connection: In many states, your credit score is a massive factor. Improving your score by even 50 points can sometimes lower your premium more than five years of safe driving.

- Paperless & Paid-in-Full: It’s 2026. If you’re still receiving paper bills in the mail, you’re likely paying a “convenience fee” for the privilege. Switching to digital and paying six months upfront can save you a chunk of change.

High-Risk vs. High-Value: Finding the Middle Ground

We often see people make the mistake of choosing “cheap” over “affordable.” Cheap insurance is great until you realize your liability limits are so low that a fender bender with a luxury SUV puts your entire life savings at risk.

Finding the best affordable car insurance means balancing the premium with the protection. For example, if you live in Maine, you might think you’re saving money by skipping comprehensive coverage until a moose decides your hood is a great place to sit. At that point, “cheap” becomes very expensive.

Quick Comparison: Coverage vs. State Realities (2026)

| State | Mandatory Minimums | The “Smart” Choice | Why? |

| Arizona | 25/50/15 | Add Full Glass | Dust storms & haboobs = cracked windshields. |

| Maine | 50/100/25 | Add Animal Strike | Deer and moose don’t care about your deductible. |

| West Virginia | 25/50/25 | Higher Collision | Icy mountain roads are unforgiving to bumpers. |

| Wyoming | 25/50/20 | Comprehensive | Ground blizzards can cause “Acts of God” damage. |

How to Win the “Quote War”

The best way to ensure you aren’t overpaying is to create a “Quote War.” When you use a platform like Easy Car Quotes, you aren’t just looking at one price. You’re forcing multiple carriers to bid for your business.

Think of it like a dating app, but instead of looking for a soulmate, you’re looking for someone who won’t charge you $300 a month because you live in a zip code with a lot of potholes.

The 3-Step Strategy for 2026:

- Audit Your Mileage: Are you still working from home three days a week? If your annual mileage has dropped from 15,000 to 5,000, your insurance company needs to know. You’re a lower risk now.

- Adjust Your Deductible: If you have $1,000 in an emergency fund, stop carrying a $250 deductible. Raising it to $500 or $1,000 can drop your monthly premium significantly.

- Compare Every 6 Months: Loyalty is for dogs, not insurance companies. Check the market twice a year to ensure your “good driver” status is actually being rewarded.

Why Your Location Matters (More Than You Think)

Your neighbor might have the best affordable car insurance through Provider A, but because your car is parked in a garage and theirs is on the street, Provider B might be better for you.

Insurance companies are obsessed with data. They look at crime rates, weather patterns, and even how many people in your area filed claims for hail damage last year. This is why using a localized search tool is vital. It’s not just about being in “Arizona” it’s about being in “Scottsdale vs. Tucson.”

The Final Verdict: Is It Worth the Effort?

In a world where the cost of living seems to go up every time you blink, car insurance is one of the few recurring bills you actually have control over. You can’t control the price of eggs, but you can control what you pay to protect your vehicle.

By spending fifteen minutes comparing options, most drivers find they can save hundreds of dollars a year. That’s money that could go toward a vacation, a new tech gadget, or just a really, really fancy dinner where you don’t have to look at the prices.

Ready to Stop Overpaying?

Don’t let another month go by with an “autopilot” premium. Secure your finances and get back on the road with confidence.